Thought Leadership

Leaders in business and STEM

Relevance

Novel and pertinent titles

Global

Tens of cities around the world

Leaders in business and STEM

Novel and pertinent titles

Tens of cities around the world

Ever since our first Thalesian Seminar in London, which took place on 2009.01.29, the Thalesians have been organizing industry-leading seminars in tens of cities around the world.

The focus of the Thalesian Seminar series is on quantitative finance, analysis, and development; machine learning and artificial intelligence; high-performance computing; and, more broadly, science, technology, engineering, and mathematics.

Our meticulously chosen Thalesian Speakers are thought leaders in their respective fields; they are at the forefront of the academia and/or industry. The Thalesian Speakers have included some of the most famous names in machine learning, electronic trading, quantitative finance, and more broadly, mathematics, computer science, engineering, finance, economics, and psychology.

The Thalesian Seminars are administered via Meetup.com. To attend, please register on the Thalesians Meetup.

| Number | Date | Location | Partner | Venue | Speaker | Title |

|---|---|---|---|---|---|---|

| 436 | 2025-02-04 | New York, hybrid | IAQF | Fordham University | Dan Pirjol | Total Positivity and TP2 Violations in Option Markets |

| 435 | 2025-01-14 | New York, hybrid | IAQF | Fordham University | Agostino Capponi | Stress Testing Spillover Risk in Mutual Funds |

| 434 | 2024-12-18 | London | First Derivatives, FirstRate Data, G-Research, Hudson & Thames, KX Systems, Turnleaf Analytics, Packt | City University Club | Dr Paul Alexander Bilokon | The Thalesians Festive Dinner, Optimal Allocation of Resources in Nonstationary Conditions |

| 433 | 2024-12-03 | New York, hybrid | IAQF | Fordham Univesity | Frédéric Godin | Enhancing Deep Hedging of Options |

| 432 | 2024-11-04 | New York, hybrid | IAQF | Fordham University | Dr Ilia Bouchouev | Talk and Book Signing: Virtual Barrels: Quantitative Trading in Oil Market |

| 431 | 2024-10-29 | London | First Derivatives, FirstRate Data, G-Research, Hudson & Thames, KX Systems, Turnleaf Analytics, Packt | G-Research headquarters | Prof. Johannes Muhle-Karbe | The Cost of Misspecifying Price Impact |

| 430 | 2024-10-07 | New York, hybrid | IAQF | Fordham University | Luca Capriotti | Quants, Quantum Mechanics and Quantos |

| 429 | 2024-09-24 | London | First Derivatives, FirstRate Data, G-Research, Hudson & Thames, KX Systems, Turnleaf Analytics, Packt | G-Research headquarters | Prof. Antoine (Jack) Jacquier | Building volatility models from data |

| 428 | 2024-09-10 | New York, hybrid | IAQF | Fordham University | Valentin Tissot-Daguette | Capturing Path Dependence in Finance |

| 427 | 2024-06-05 | London | Thalesians Marine Ltd | Idea Store Whitechapel | Oleksandr Bilokon | Book signing: A Brief History of Artificial Intelligence and AI in Shipping |

| 426 | 2024-05-29 | London | First Derivatives, FirstRate Data, G-Research, Hudson & Thames, KX Systems, Turnleaf Analytics, Packt | G-Research headquarters | Victor Haghani | Missing Billionaires: Bernoulli, von Neumann to Taleb |

| 425 | 2024-05-07 | New York, hybrid | IAQF | G-Research headquarters | Marian Gidea | Topological Data Analysis Detects Financial Bubbles |

| 424 | 2024-04-11 | London | First Derivatives, FirstRate Data, G-Research, Hudson & Thames, KX Systems, Turnleaf Analytics, Packt | G-Research headquarters | Dr Ilia Bouchouev | Virtual Barrels: Quantitative Trading in Oil Market |

| 423 | 2024-04-09 | New York, hybrid | IAQF | Fordham University | Dacheng Xiu | Expected Returns and Large Language Models |

| 422 | 2024-03-05 | New York, hybrid | IAQF | Fordham University | Stan Uryasev | Risk Quadrangle Theory and Applications |

| 421 | 2024-02-06 | New York, hybrid | IAQF | Fordham University | Dr Samim Ghamami | Risk Analysis of Central Counterparties |

| 420 | 2024-01-18 | Canary Wharf, London, hybrid | World Business Strategies (WBS Training), Machine Learning Institute (MLI), Quantitative Developer Certificate (QDC) | Level39 | Saeed Amen, Paul Bilokon, Blanka Horvath, Ryan Siegler, Abir Sridi, Olga Petrova | Financial AI and Software Development in the Era of ChatGPT and Quantum Computing |

| 419 | 2024-01-10 | Paris | Le Rocroy Hotel - Les Espaces Rocroy | Mehdi Tomas | Crossimpact: Whent to bother and how to model it | |

| 418 | 2024-01-09 | New York, hybrid | IAQF | Fordham University | Dr Pawel Polak | Enseble Models for Optimal Predictive Performance |

| 417 | 2024-01-08 | Sant Cugat (near Barcelona) | AC Hotel by Marriott Sant Cugat | Prof. Elisa Alòs | Local and implied volatility via Malliavin calculus | |

| 416 | 2023-12-13 | London | G-Research, KX Systems, Turnleaf Analytics, Packt | Online | Ryan Siegler | GenAI, RAG & Vector Databases |

| 415 | 2023-12-05 | New York, hybrid | IAQF | Fordham University | Dr Cristian Bravo | Leveraging Deep Learning for Multimodal Data Analysis in Credit Risk Assessment |

| 414 | 2023-11-14 | New York, hybrid | IAQF | Fordham University | Ciamac Moallemi | Automated Market Making and Decentralized Exchanges |

| 413 | 2023-11-08 | London, G-Research | G-Research, KX Systems, Turnleaf Analytics | G-Research headquarters | Robert Carver | The Futures Trend Following Strategy |

| 412 | 2023-10-25 | London, G-Research | G-Research, KX Systems, Turnleaf Analytics | G-Research headquarters | Eyal Neuman | Offline/Online Learning Approaches to Price Impact Models |

| 411 | 2023-10-03 | New York, hybrid | IAQF | Fordham University | Matheus Venturyne Xavier | Credible Decentralized Exchange Design |

| 410 | 2023-09-13 | London, G-Research | G-Research, KX Systems, Turnleaf Analytics | G-Research headquarters | Vladimir V. Piterbarg | Alternatives to Deep Neural Networks in Finance |

| 409 | 2023-09-12 | New York, hybrid | IAQF | Fordham University | Pedro Tremacoldi-Rossi | Bias of Simple Bid-Ask Spread Estimators |

| 408 | 2023-06-13 | New York, hybrid | IAQF | Fordham University | Lin Peng | Social Ties, Comovements, and Predictable Returns |

| 407 | 2023-05-24 | London, G-Research | G-Research, KX Systems, Turnleaf Analytics | G-Research headquarters | Blanka Horvath | Detecting Regime Shifts in Financial Markets |

| 406 | 2023-05-09 | New York, hybrid | IAQF | Fordham University | Liuren Wu | Common Pricing of Decentralised Risk |

| 405 | 2023-04-18 | New York, hybrid | IAQF | Fordham University | Shivaram Rajgopal | Rethinking Value and Implications of Green Bonds |

| 404 | 2023-03-29 | London, G-Research | G-Research, KX Systems, Turnleaf Analytics | G-Research headquarters | Saeed Amen and Alexander Denev | Inflation Forecasting with ML |

| 403 | 2023-03-22 | New York, hybrid | IAQF | Fordham University | Igor Haperin | Reinforcement and Inverse Reinforcement Learning |

| 402 | 2023-02-14 | New York, hybrid | IAQF | Fordham University | Sasha Stoikov | Where Market Making Meets Market Microstructure |

| 401 | 2023-01-24 | New York, hybrid | IAQF | Fordham University | Peng Cheng | Equity Alpha Signals From High Frequency Option Data |

| 400 | 2022-12-13 | New York, hybrid | IAQF | Fordham University | Sudip Gupta | Financial inclusion and alternative credit scoring |

| 399 | 2022-11-15 | New York, hybrid | IAQF | Fordham University | Nicholas Westray | Deep Order Flow Imbalance |

| 398 | 2022-11-02 | London, remote | Warren B. Powell | From Reinforcement Learning to Sequential Decisions | ||

| 397 | 2022-10-24 | New York, hybrid | IAQF | Fordham University | Gordon Ritter | Optimal Turnover, Liquidity, and Autocorrelation |

| 396 | 2022-09-07 | London | QDC | Level39 | Paul Bilokon | Databases in finance: beyond SQL, towards BD and HFT |

| 395 | 2022-08-17 | London | QDC | Level39 | Saeed Amen | Visualisation for financial markets in Python |

| 394 | 2022-08-10 | London | MLI | Level39 | David Foster | DALL.E 2: Text-to-image generation |

| 393 | 2022-07-19 | London | Level39 | Hudson & Thames | Evening Conference on Algorithmic Trading and ML | |

| 392 | 2022-06-28 | New York, online | IAQF | Online | Michael Kearns | Differentially Private Call Auctions and Market Impact |

| 391 | 2022-05-23 | New York, online | IAQF | Online | Stan Uryasev | Drawdown Beta and Portfolio Optimization |

| 390 | 2022-04-20 | London, online | Online | Uwe Wystup | Mixed Local Volatility Models for FX Derivatives | |

| 389 | 2022-04-12 | New York, online | IAQF | Online | Jan W. Dash | Climate Change: Opportunity and Risk |

| 388 | 2022-03-08 | New York, online | IAQF | Online | Magnus Wiese | Multi-Asset Option Market Simulation |

| 387 | 2022-02-08 | New York, online | IAQF | Online | Ruixun Zhang | Quantifying the Impact of Impact Investing |

| 386 | 2022-01-26 | London, online | Online | Ira Baxter | Automated transformation for software engineering using DMS | |

| 385 | 2022-01-10 | New York, online | IAQF | Online | Miquel Noguer i Alonso | Deep Learning for Equity Time Series Prediction |

| 384 | 2021-12-08 | London, online | Online | Agatha Murgoci | Time Inconsistent Optimal Control in Finance | |

| 383 | 2021-11-17 | New York, online | IAQF | Online | Andrew Kalotay | Measuring and Maximizing After-Tax Performance |

| 382 | 2021-11-10 | New York, online | IAQF | Online | Andrea Barbon | Gamma Fragility |

| 381 | 2021-10-27 | London, online | Online | Marek Capinski | Three stories on mathematical finance | |

| 380 | 2021-10-18 | New York, online | IAQF | Online | Agostino Capponi | Adoption of Blockchain-Based Decentralized Exchanges |

| 379 | 2021-10-13 | London, online | Online | Bruno Bouchard-Denize | Dupire-Ito's formula for C^{0,1} functionals | |

| 378 | 2021-09-22 | London, online | Online | Bilal Hafeez | How Macro Can Help Quants | |

| 377 | 2021-09-13 | New York, online | IAQF | Online | Eric Talley | Cleaning Corporate Governance |

| 376 | 2021-09-02 | London, online | Online | Alec Schmidt | Diversifying Mean-Variance Portfolio: Physics versus Mathematics | |

| 375 | 2021-08-25 | London, online | Online | Daniel J. Duffy | PDEs and FDM for Computational Finance | |

| 374 | 2021-08-18 | London, online | Online | Mehdi Tomas | How to model time-dependent multivariate price impact | |

| 373 | 2021-08-11 | London, online | Online | Viral Shah and Matt Bauman | High performance financial computing with JuliaHub | |

| 372 | 2021-07-28 | London, online | Online | Thomas Spooner | Market Making, Reinforcement Learning, and Uncertainty | |

| 371 | 2021.07.21 | London | Online | Olga Petrova | Introduction to Transformers for NLP | |

| 370 | 2021.07.14 | London | Online | Ashwin Rao | Foundations of Reinforcement Learning with Applications to Finance | |

| 369 | 2021.06.30 | London | Online | Elisa Alòs Alcalde | Malliavin Calculus in Finance: Theory and Practice | |

| 368 | 2021.06.23 | London | Online | Gianluca De Nard | Oops! I Shrunk the Sample Covariance Matrix Again: Blockbuster Meets Shrinkage | |

| 367 | 2021.06.16 | London | Online | Nick Psaris | Fun Q: A Functional Introduction to ML in kdb+/q | |

| 366 | 2021.06.07 | New York | IAQF | Online | Jean-Marc Mercier | A Class of Mesh-free Algorithms for Finance, Machine Learning, and Fluid Dynamics |

| 366 | 2021.06.07 | New York | IAQF | Online | Philippe G. LeFloch | Machine Learning, and Fluid Dynamics |

| 365 | 2021.06.02 | London | Online | Colin Lancaster | Fed Up!: Success, Excess and Crisis Through the Eyes of a Hedge Fund Macro Trader | |

| 364 | 2021.05.19 | London | Online | Jörg Kienitz | Data Driven and Model Free Conditional Expectations - DCKE Method | |

| 363 | 2021.05.10 | New York | IAQF | Online | Daniel Rabetti | Coins for Bombs: Detecting Terrorist Attack Funding with Cryptocurrencies |

| 362 | 2021.04.19 | New York | IAQF | Online | Joseph Simonian | Modular Machine Learning: The Best of Both Worlds? |

| 361 | 2021.04.07 | London | Online | Masaaki Fukasawa | Volatility Has to Be Rough | |

| 360 | 2021.03.31 | London | Online | Piotr Karasinski | Random Walk from Physics to Finance: to Yale, Wall Street, and the City of London from Behind the Iron Curtain | |

| 359 | 2021.03.10 | London | Online | Irene Aldridge | Noise Dynamics in Big Data Inference: How Missing Observations Affect (And Do Not Affect) Quality of Analysis | |

| 358 | 2021.03.08 | New York | IAQF | Online | Rainer Hirk | Joint Model of Failures & Credit Ratings |

| 357 | 2021.03.03 | London | Online | Rob Carver | Risk Targeting: Infinity War | |

| 356 | 2021.02.24 | London | Online | Jesper Andreasen (Kwant Daddy) | Next Generation Local Volatility | |

| 355 | 2021.02.17 | London | Online | Brian Norsk Huge | AAD and Differential Machine Learning | |

| 355 | 2021.02.17 | London | Online | Antoine Savine | AAD and Differential Machine Learning | |

| 354 | 2021.02.10 | London | Online | Rolf Poulsen | Tales of Innumeracy | |

| 353 | 2021.02.08 | New York | IAQF | Online | Ioannis Anagnostou | Contagious Defaults in a Credit Portfolio: A Bayesian Network Approach |

| 352 | 2021.01.27 | London | Online | Martin Tegner | A Probabilistic Machine Learning Approach to Local Volatility | |

| 351 | 2021.01.20 | London | Online | Alexander Tsyplikhin | MIMD Architecture and Opportunities for AI/ML Optimisation in Finance using IPUs | |

| 351 | 2021.01.20 | London | Online | Andrew Addison | MIMD Architecture and Opportunities for AI/ML Optimisation in Finance using IPUs | |

| 350 | 2021.01.13 | London | Online | Jochen Papenbrock | Explainable, Accelerated Machine Intelligence | |

| 349 | 2021.01.11 | New York | IAQF | Online | Yoshihiro Tawada | Machine Learning Hedge Strategy with Deep Gaussian Process Regression |

| 348 | 2020.12.14 | New York | IAQF | Online | Elliott Ash | A Machine Learning Approach to Analyze and Support Anti-Corruption Policy |

| 347 | 2020.12.09 | London | Online | Thomas Wiecki | Bayesian Portfolio Construction | |

| 346 | 2020.12.02 | London | Online | Johannes Ruf | Hedging with Linear Regressions and Neural Networks | |

| 345 | 2020.11.30 | New York | IAQF | Online | Mark Jansen | Human versus Machine: Underwriting Decisions in Finance |

| 344 | 2020.11.25 | London | Online | Christina Qi | Starting a Modern Hedge Fund | |

| 343 | 2020.11.18 | London | Online | Robin Wigglesworth | Passive Aggressive: Birth, Growth, and Future of Index Investing | |

| 342 | 2020.11.11 | London | Online | Cetin Karakus | Anatomy of a Distributed Options Market Making System | |

| 341 | 2020.10.29 | London | Online | Michael Imerman | Pandemic Exposure, Credit Market Reaction, Corporate Default Risk | |

| 340 | 2020.10.28 | New York | IAQF | Online | Corey Weistuch | Learning Complex Dynamical Patterns from Simple Models |

| 339 | 2020.10.21 | London | Online | Uri Lee | Complex Networks in Finance | |

| 338 | 2020.10.21 | London | Online | David Munoz Constantine | Synthetic Data Generation with MlFinLab | |

| 337 | 2020.10.21 | London | Online | Valeriia Pervushyna | Statistical Arbitrage with the Ornstein-Uhlenbeck Model | |

| 336 | 2020.10.14 | London | Online | Ryan Ferguson | Recent Progress in Accelerating Derivatives Models | |

| 335 | 2020.10.07 | London | Online | David Foster | Generative Deep Learning - The Key to Unlocking AGI | |

| 334 | 2020.09.30 | London | Online | Jens Nordvig | Forecasting the Dollar Using Capital Flow Data | |

| 333 | 2020.09.29 | New York | IAQF | Online | Bud Mishra | Seeking the Self amidst COVID's Cytokine Cyclones |

| 332 | 2020.09.23 | London | Online | Luigi Ballabio | A Short Introduction to QuantLib | |

| 331 | 2020.09.16 | London | Online | Grady Booch | Software Architecture for AI-intensive Systems | |

| 330 | 2020.09.09 | London | Online | Jay Cao | Deep Hedging Using RL | |

| 330 | 2020.09.09 | London | Online | Jacky Chen | Deep Hedging Using RL | |

| 330 | 2020.09.09 | London | Online | John Hull | Deep Hedging Using RL | |

| 330 | 2020.09.09 | London | Online | Zissis Poulos | Deep Hedging Using RL | |

| 329 | 2020.09.02 | London | Online | Alexander Denev | The Book of Alternative Data | |

| 328 | 2020.09.02 | London | Online | Saeed Amen | The Book of Alternative Data | |

| 327 | 2020.08.19 | London | Online | Maria Grazia Vigliotti | The Executive Guide to Blockchain | |

| 326 | 2020.08.13 | London | Online | Matthew Dixon | ML in Finance | |

| 326 | 2020.08.13 | London | Online | Igor Halperin | ML in Finance | |

| 326 | 2020.08.13 | London | Online | Paul Bilokon | ML in Finance | |

| 325 | 2020.08.12 | London | Online | Ernest Chan | Tail Hedging in the Age of Machine Learning | |

| 324 | 2020.08.05 | London | Online | Daniel Duffy | Some Perspectives on Computational Finance and ML | |

| 323 | 2020.07.16 | London | Online | Daniele Bernardi | Bitcoin's Price Prediction | |

| 322 | 2020.07.09 | London | Online | Jörg Kienitz | General Stochastic Volatility - New Models and DNN | |

| 321 | 2020.07.08 | London | Online | Alex Zhavoronkov | Machine Learning and Drug Discovery | |

| 320 | 2020.06.24 | London | Online | Tomas Sabat | Grakn & Query Language in Finance and Drug Discovery | |

| 319 | 2020.06.17 | London | Online | Bharath Ramsundar | Machine Learning and the Fight against COVID-19 | |

| 318 | 2020.06.16 | New York | IAQF | Online | Petter Kolm | Greedy Online Classification of Persistent Market States |

| 317 | 2020.06.11 | London | Online | Markus Hofer | Quantifying Systemic Risk using Bayesian Statistics | |

| 316 | 2020.06.03 | London | Online | Marcos López de Prado | ML Solutions to Bias-Variance Dilemma | |

| 315 | 2020.05.28 | London | Online | Nikolaus Hautsch | Limits to Arbitrage in Blockchain-Based Markets | |

| 314 | 2020.05.21 | London | Online | Jason Tatton | The Concurnas Programming Language | |

| 313 | 2020.05.14 | London | Online | Blanka Horvath | A Data-driven Market Simulator | |

| 312 | 2020.05.06 | London | Online | Yves Hilpisch | RL: From Games to Intraday Algorithmic Trading | |

| 311 | 2020.05.05 | New York | IAQF | Online | Josef Teichmann | Deep Hedging |

| 310 | 2020.04.30 | London | Online | Matthew Dixon | Deep Local Volatility | |

| 309 | 2020.04.23 | London | Online | Mehdi Tomas | How to Build a Cross-Impact Model from First Principles | |

| 308 | 2020.04.16 | London | Online | Alexandre Antonov | Neural Networks with Asymptotics Control | |

| 307 | 2020.04.08 | London | Online | Claudio Albanese | Model Risk and Reverse Stress Testing | |

| 306 | 2020.04.06 | New York | IAQF | Online | Jonathan Schachter | Weaning Ourselves Off LIBOR |

| 305 | 2020.03.02 | New York | IAQF | Fordham University Gabelli School of Business | Ryan Ferguson | Deeply Learning Derivatives |

| 304 | 2020.02.26 | London | Level39 | David Hand | Dark Data, What You Don't Know, Why It Matters, What to Do about It | |

| 303 | 2020.02.03 | New York | IAQF | Fordham University Gabelli School of Business | Stephan Sturm | Portfolio Selection Using the Distribution Builder |

| 302 | 2020.01.27 | London | Informa | Informa/EPFR | Greg Zuckerman | Book Talk on Renaissance Technologies: Jim Simons - The Man Who Solved the Market |

| 301 | 2020.01.15 | London | Level39 | Ulrich Nogel | It's all about Liquidity - Europe Cash Equity Trading Trends | |

| 300 | 2020.01.07 | New York | IAQF | Fordham University Gabelli School of Business | Andrew Papanicolaou | PCA for Implied Volatility Surfaces |

| 299 | 2019.12.10 | New York | IAQF | Fordham University Gabelli School of Business | Keywan Rasekhschaffe | Machine Learning for Stock Selection |

| 298 | 2019.12.09 | London | Level39 | Jan Novotny | Machine Learning and Big Data with kdb+/q | |

| 297 | 2019.11.20 | London | London Marriott Hotel Canary Wharf | Mark Salmon | The Importance of Causal Machine Learning in Asset Management | |

| 296 | 2019.11.05 | New York | IAQF | Fordham University Gabelli School of Business | Rajesh T. Krishnamachari | Big Data and AI Strategies |

| 295 | 2019.10.30 | London | London Marriott Hotel Canary Wharf | Sayad Baronyan | Fund Flows and Allocations as Predictors of Asset Returns | |

| 294 | 2019.10.16 | New York | IAQF | Fordham University Gabelli School of Business | Kevin Noel | Systematic Strategies and Machine Learning |

| 293 | 2019.09.25 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Making Python Parallel with Large Datasets | |

| 292 | 2019.09.10 | New York | IAQF | Fordham University Gabelli School of Business | Ricardo A. Collado | Time Series Forecasting with a Learning Algorithm |

| 291 | 2019.09.05 | Vienna | University of Vienna | Christian Donninger | From the Chess Monster Hydra to VIX Futures Trading | |

| 290 | 2019.07.17 | London | London Marriott Hotel Canary Wharf | Abbas Edalat | Algorithmic Human Development | |

| 289 | 2019.06.26 | London | London Marriott Hotel Canary Wharf | Fernando de Meer | Machine Learning to Create Synthetic Financial Time Series | |

| 288 | 2019.06.11 | New York | IAQF | Fordham University Gabelli School of Business | Matthew Dixon | Blockchain Analytics for Intraday Financial Risk Modelling |

| 287 | 2019.05.22 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Introduction to Natural Language Processing | |

| 286 | 2019.05.16 | Vienna | University of Vienna | Slawek Smyl | Machine Learning in Time Series Forecasting created by Uber Engineering | |

| 285 | 2019.05.07 | New York | IAQF | Fordham University Gabelli School of Business | Paolo Guasoni | Options Portfolio Selection |

| 284 | 2019.04.24 | London | King's College London | Blanka Horvath | Deep Learning Volatility | |

| 283 | 2019.04.08 | New York | IAQF | Fordham University Gabelli School of Business | Terry Benzschawel | Financial Applications of Machine Learning |

| 282 | 2019.03.26 | London | London Marriott Hotel Canary Wharf | Marcos Carreira | Learning Interest Rate Interpolation | |

| 281 | 2019.03.13 | London | City University Club | Dilip Madan | Risk Management using the Valuation of Risk Exposure Variation | |

| 280 | 2019.03.12 | New York | IAQF | Fordham University Gabelli School of Business | Dmitriy Muravyev | Using Options to Explain Short Selling Returns |

| 279 | 2019.02.26 | London | London Marriott Hotel Canary Wharf | Douglas Machado Vieira | High-frequency Options Market Making and Stochastic Volatility | |

| 278 | 2019.02.18 | London | Level39 | Paul Bilokon | Workshop: Introduction to Data Science and Machine Learning | |

| 277 | 2019.02.12 | New York | IAQF | Fordham University Gabelli School of Business | Yixiao (Ethan) Jiang | Semiparametric Estimation of a Credit Rating Model |

| 276 | 2019.01.30 | London | London Marriott Hotel Canary Wharf | Rama Cont | Flash Crash: Algorithmic Execution and Market Dynamics | |

| 275 | 2019.01.15 | New York | IAQF | Fordham University Gabelli School of Business | Joy Zhang | Agency MBS Prepayment Model using Neural Networks |

| 274 | 2018.12.11 | New York | IAQF | Fordham University Gabelli School of Business | R. Douglas Martin | Fama-French 1992 Redux with Robus Statistics |

| 273 | 2018.12.10 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Saeed Amen | Annual Festive Dinner Talk: Trading Thalesians |

| 273 | 2018.12.10 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Paul Bilokon | Annual Festive Dinner Talk: Neocybernetics |

| 273 | 2018.12.10 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Dario Scarcella | Annual Festive Dinner Talk: Blockchain and a Decentralized Debt Capital Market |

| 272 | 2018.11.21 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Rob Carver | Portfolio Optimization with Uncertainty |

| 271 | 2018.11.14 | New York | IAQF | NYU Kimmel Center | Gordon Ritter | The Usefulness of Reinforcement Learning in Finance |

| 270 | 2018.10.24 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Swati Mital | Equity Derivatives Trading and Modelling |

| 269 | 2018.10.15 | New York | IAQF | Fordham University Gabelli School of Business | Marzena Rostek | Financial Innovation in Decentralized Markets |

| 268 | 2018.10.10 | London | Techila Technologies | City University Club | Pasquale Della Corte | Cross-Section of Currency Volatility Premia |

| 267 | 2018.09.19 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Bjorn Stiel | Making Python Parallel, Distributing Monte Carlo with Celery |

| 266 | 2018.09.04 | New York | IAQF | NYU Kimmel Center | Arik Ben Dor | The Low Volatility Phenomenon across the Capital Structure |

| 265 | 2018.07.25 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Esther Wershof | Explaining and Stopping Pattern Formation in Tumours |

| 264 | 2018.07.11 | London | Techila Technologies | City University Club | Sophie Bismuth | Quantum Computation: Basics and Applications |

| 263 | 2018.07.27 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Damiano Brigo | Rogue Traders with S-shaped Utility versus VaR and Expected Shortfall |

| 262 | 2018.06.20 | New York | IAQF | NYU Kimmel Center | Kasper Larsen | Smart TWAP Trading in Continuous-Time Equilibria |

| 261 | 2018.06.13 | London | Techila Technologies | City University Club | Ian Khrashchevskyi | Is There a Reward for Macroeconomic Risk in Higher Moment Risk Premia? |

| 260 | 2018.05.30 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Svetlana Borovkova | AI: Sentiment in News and Social Media for Investment and Trading |

| 259 | 2018.05.28 | Vienna | University of Vienna | Douglas Machado Vieira | Machine Learning in Finance | |

| 259 | 2018.05.28 | Vienna | University of Vienna | Ivan Zhdankin | Machine Learning in Finance | |

| 258 | 2018.05.15 | New York | IAQF | NYU Kimmel Center | Albert S. Kyle | The Market Impact Puzzle |

| 257 | 2018.04.25 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Paula Rowińska | What's behind My Energy Bill? |

| 256 | 2018.04.09 | New York | IAQF | Fordham University Gabelli School of Business | Leif Andersen | Funding and Counterparty Credit Costs |

| 255 | 2018.03.21 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Blanka Horvath | Volatility Is Rough? Just Learn It! |

| 254 | 2018.03.15 | New York | IAQF | NYU Kimmel Center | Celso Brunetti | Common Holdings and Systemic Risk |

| 253 | 2018.02.22 | New York | IAQF | NYU Kimmel Center | Ronnie Sircar | Stochastic and Implied Sharpe Ratio |

| 252 | 2018.02.22 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Paul Bilokon | Workshop: Data Science, Machine Learning, and Python |

| 251 | 2018.02.21 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Paul Bilokon | From AI to ML, from Logic to Probability |

| 250 | 2018.01.24 | London | Techila Technologies | London Marriott Hotel Canary Wharf | Giles Heywood | UK Residential Property Modelling |

| 249 | 2018.01.09 | New York | IAQF | NYU Kimmel Center | Alexander Veygman | Jump on Default for Multiple Default Contingent Claims |

| 248 | 2017.12.11 | London | London Marriott Hotel Canary Wharf | Tomaso Aste | Annual Festive Dinner Talk: Can Artificial Intelligence Predict the Behaviour of Markets and Societies? | |

| 247 | 2017.12.05 | New York | IAQF | Bank of China | Lasse Pedersen | Generalized Recovery |

| 246 | 2017.11.22 | London | London Marriott Hotel Canary Wharf | Douglas Machado Vieira | Optimal Market Making across Assets | |

| 245 | 2017.11.15 | London | London Marriott Hotel Canary Wharf | Jochen Papenbrock | Financial Networks and AI | |

| 244 | 2017.11.15 | New York | IAQF | NYU Kimmel Center | Andrey Itkin | Modelling Stochastic Skew of FX Options |

| 243 | 2017.11.09 | London | City University Club | Blanka Horvath | Rough Volatility Models: Pricing and Simulations | |

| 242 | 2017.10.25 | London | London Marriott Hotel Canary Wharf | Mark Davis | Model-Free Finance | |

| 241 | 2017.10.11 | London | City University Club | Malcolm Sherrington | Fractals, Finance, and Fractured Fairy Tales | |

| 240 | 2017.10.10 | New York | IAQF | NYU Kimmel Center | David Zhang | Model House Price Volatility |

| 239 | 2017.09.27 | London | London Marriott Hotel Canary Wharf | Justin Chan | Forward Simulating Initial Margin with AAD | |

| 238 | 2017.09.12 | New York | IAQF | NYU Kimmel Center | David Shimko | Total Risk and Project Valuation |

| 237 | 2017.09.06 | London | City University Club | Jason Ricci | Stochastic Control in Algorithmic Trading | |

| 236 | 2017.07.05 | London | Level39 | Paul Bilokon | The Moon, the Robot, and Python | |

| 235 | 2017.06.26 | London | London Marriott Hotel Canary Wharf | Harvey Stein | Big Data's Dirty Secret | |

| 234 | 2017.06.14 | San Francisco | Quiota | Keiran Thompson | Gaussian Processes for Portfolio Optimization | |

| 233 | 2017.06.14 | New York | IAQF | NYU Kimmel Center | Harrison G. Hong | Climate Risks and Market Efficiency |

| 232 | 2017.06.07 | London | City University Club | Frank Berkshire | Chaotic Cards/Dynamic Dice: Profitable, but Risky | |

| 231 | 2017.05.24 | London | London Marriott Hotel Canary Wharf | Lynda White | Life Is a Game! | |

| 230 | 2017.05.15 | New York | IAQF | NYU Kimmel Center | Sebastian Jaimungal | Trading Algorithms with Learning in Alpha Models |

| 229 | 2017.04.26 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Flash People - Introduction to HFT | |

| 228 | 2017.04.26 | Stockholm | Kräftriket | Paul Bilokon | Bayesian Methods in Electronic Trading | |

| 227 | 2017.04.25 | New York | IAQF | NYU Kimmel Center | Andrew Papanicolaou | Trading in VIX Derivatives |

| 226 | 2017.04.19 | London | City University Club | Marc Henrard | SIMM and SA FRTB: Algorithmic Differentiation | |

| 225 | 2017.03.29 | London | London Marriott Hotel Canary Wharf | Chris Godfrey | Behavioural Finance: Current State of Play | |

| 224 | 2017.03.16 | New York | IAQF | NYU Kimmel Center | Lingjiong Zhu | A Reduced-Form Model for Level-1 Limit Order Books |

| 223 | 2017.03.13 | San Francisco | Quiota | Steve Pav | The Pitfalls of Backtesting | |

| 223 | 2017.03.13 | San Francisco | Quiota | Matthew Dixon | Queue Position and Order Flow Imbalance | |

| 223 | 2017.03.13 | San Francisco | Quiota | Scott Locklin | Predicting with Confidence | |

| 222 | 2017.03.09 | London | City University Club | Iain Clark | Efficient Methods for Simulation of FX Volatility Surface | |

| 221 | 2017.03.06 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Jacques du Toit | Innovations in Quant Finance from NAG |

| 220 | 2017.02.22 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Using Python to Analyse Financial Markets | |

| 219 | 2017.02.15 | New York | IAQF | NYU Kimmel Center | Alan Moreira | Volatility Managed Portfolios |

| 218 | 2017.01.25 | London | London Marriott Hotel Canary Wharf | Oskar Mencer | Multiscale Dataflow Risk on Hybrid Cloud | |

| 217 | 2017.01.24 | New York | IAQF | NYU Kimmel Center | Tai-Ho Wang | Probability Density of Lognormal Fractional SABR Model |

| 216 | 2016.12.14 | New York | IAQF | NYU Kimmel Center | Hongzhong Zhang | Intraday Market Making with Overnight Inventory Costs |

| 215 | 2016.12.12 | London | London Marriott Hotel Canary Wharf | Iain Clark | Annual Festive Dinner Talk: Implied Distribution of FX Risk Reversals in Brexit/Trump | |

| 214 | 2016.11.23 | London | London Marriott Hotel Canary Wharf | Vlasios Voudouris | Flexible Machine Learning for Finance | |

| 213 | 2016.11.17 | New York | IAQF | NYU Kimmel Center | Michael B. Imerman | A Data-Driven Analysis of the Volatility Risk Premium |

| 212 | 2016.10.24 | London | London Marriott Hotel Canary Wharf | David Hand | The Improbability Principle | |

| 211 | 2016.10.20 | New York | IAQF | NYU Kimmel Center | Erik Vogt | Global Variance Term Premia and Intermediary Risk Appetite |

| 210 | 2016.09.28 | London | London Marriott Hotel Canary Wharf | Nick Baltas | Trading Multi Asset Carry | |

| 209 | 2016.09.15 | New York | IAQF | NYU Kimmel Center | Arun Verma | Statistical Arbitrage Using News and Social Sentiment |

| 208 | 2016.07.20 | London | London Marriott Hotel Canary Wharf | Scott Cogswell | Initial Margin Model | |

| 207 | 2016.06.29 | London | London Marriott Hotel Canary Wharf | Steve Hutt | Advances in Deep Learning and Usage in Markets | |

| 206 | 2016.06.16 | New York | IAQF | NYU Kimmel Center | Tobias Adrian | Nonlinearity and Flight-to-Safety |

| 205 | 2016.06.09 | Zurich | Plattenstrasse 14 | Felix Zumstein | Python in Quantitative Finance | |

| 204 | 2016.05.25 | London | London Marriott Hotel Canary Wharf | Paul Bilokon | How to Run an Electronic Market Making Business? | |

| 203 | 2016.05.12 | New York | IAQF | NYU Kimmel Center | Luis Seco | Are Negative Hedge Fund Fees on the Horizon? |

| 202 | 2016.05.11 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Thomas Wiecki | Predict Out-of-Sample Performance |

| 201 | 2016.05.09 | Budapest | InterContinental Hotel Budapest | Saeed Amen | Thalesian Workshop at Global Derivatives | |

| 200 | 2016.05.09 | Budapest | InterContinental Hotel Budapest | Paul Bilokon | Thalesian Workshop at Global Derivatives | |

| 199 | 2016.04.20 | London | London Marriott Hotel Canary Wharf | Jacob Bartram | Can Option Trading Strategies Enhance CTA/Trend Following Trading Strategies? | |

| 198 | 2016.04.14 | New York | IAQF | NYU Kimmel Center | Lawrence Glosten | Limit Order Book Tail Expectations |

| 197 | 2016.03.21 | London | Level39 | Robin Hanson | Economics when Robots Rule the Earth | |

| 196 | 2016.03.15 | New York | NYU Kimmel Center | Alexander Lipton | Modern Monetary Circuit Theory | |

| 195 | 2016.03.14 | San Francisco | Quiota | Berkeley City Club | Scott Locklin | High-performance Columnar Databases |

| 195 | 2016.03.14 | San Francisco | Quiota | Berkeley City Club | Hugh Edmundson | Data Science for Market Place Lending |

| 195 | 2016.03.14 | San Francisco | Quiota | Berkeley City Club | Matthew Dixon | Machine Learning for Algorithmic Trading |

| 194 | 2016.02.29 | London | London Marriott Hotel Canary Wharf | Jessica James | Trading FX Options | |

| 193 | 2016.02.16 | New York | IAQF | NYU Kimmel Center | Harry Mamaysky | Does Unusual News Forecast Market Stress? |

| 192 | 2016.02.08 | London | Quantopian | Thomson Reuters Building | Saeed Amen | How to Build a CTA - Creating a Trend Following Fund |

| 192 | 2016.02.08 | London | Quantopian | Thomson Reuters Building | Delaney Granizo-Mackenzie | Pair Trading Strategies |

| 191 | 2016.01.29 | Budapest | Palack Borbár | Robin Hanson | Economics when Robots Rule the Earth | |

| 190 | 2016.01.20 | London | London Marriott Hotel Canary Wharf | Nick Firoozye | Managing Uncertainty, Mitigating Risk | |

| 189 | 2016.01.12 | New York | IAQF | NYU Kimmel Center | Nick Costanzino | Pricing and Hedging Recovery Risk |

| 188 | 2015.12.14 | London | La Tasca | Matthew Dixon | Annual Festive Dinner Talk: Machine Learning in Trading | |

| 187 | 2015.12.14 | New York | IAQF | NYU Kimmel Center | Yakov Amihud | The Pricing of the Illiquidity Factor's Systematic Risk |

| 186 | 2015.11.26 | Zurich | Plattenstrasse 14 | Thomas Schmelzer | Portfolio Optimization, Regression, and Conic Programming | |

| 185 | 2015.11.25 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Global Macro Markets Discussion | |

| 184 | 2015.11.12 | New York | IAQF | NYU Kimmel Center | Andrey Itkin | Efficient Solution of Structural Default Models |

| 183 | 2015.10.21 | London | London Marriott Hotel Canary Wharf | Robert Carver | Lessons from Systematic Trading | |

| 182 | 2015.10.14 | New York | IAQF | NYU Kimmel Center | Dan Pirjol | Can One Price Eurodollar Futures in Black-Derman-Toy? |

| 181 | 2015.10.09 | Budapest | Palack Borbár | Taylor Spears | On the Sociology of CVA | |

| 180 | 2015.10.01 | New York | IAQF | Shark Tank, Grind Broadway, 22nd Floor | Saeed Amen | Creating Trend Following Fund / PyThalesians Demo |

| 179 | 2015.09.23 | London | London Marriott Hotel Canary Wharf | Stephen Pulman | Multi-Dimensional Sentiment Analysis | |

| 178 | 2015.09.21 | New York | IAQF | NYU Kimmel Center | Agostino Capponi | Arbitrage-Free Pricing of XVA |

| 177 | 2015.09.10 | San Francisco | Quiota | Berkeley City Club | Steven Pav | Portfolio Inference and Portfolio Overfit |

| 176 | 2015.09.08 | Zurich | ETH Swiss Federal Institute of Technology | Saeed Amen | Creating a Trend Following Fund / Python Demo | |

| 175 | 2015.09.07 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Saeed Amen | Quant Trading in FX and PyThalesians |

| 175 | 2015.09.07 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Jochen Papenbrock | Correlation Networks |

| 175 | 2015.09.07 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Miguel Vaz | Networks with Python/Spark |

| 175 | 2015.09.07 | Frankfurt | Quant Finance Germany Group (QFGG) | PPI AG Office | Adrian Zymolka | Multi-Period Optimization |

| 174 | 2015.07.22 | London | London Marriott Hotel Canary Wharf | Paul Bilokon | Stochastic Filtering in Electronic Trading | |

| 173 | 2015.07.15 | Budapest | Palack Borbár | Bruce Packard | Emerging Alternative Finance | |

| 172 | 2015.07.18 | New York | IAQF | NYU Kimmel Center | Tim Leung | Exchange-Traded Funda and Related Trading Strategies |

| 171 | 2015.06.17 | London | AHL | AHL | Saeed Amen | Using Python to Build Trading Strategies |

| 170 | 2015.06.03 | Frankfurt | Quant Finance Germany Group (QFGG) | Die Zentrale | Saeed Amen | Trading Thalesians Book Talk / Python FX Intraday Demo |

| 169 | 2015.05.29 | Prague | Konferenční sály Akademie věd ČR | Saeed Amen | Trading Thalesians Book Talk / Python FX Intraday Demo | |

| 168 | 2015.05.27 | London | London Marriott Hotel Canary Wharf | Artur Sepp | Gaining the Alpha Advantage in Volatility Trading | |

| 167 | 2015.05.14 | New York | IAQF | NYU Kimmel Center | Andrew Kalotay | Tax-Efficient Trading of Municipal Bonds |

| 166 | 2015.04.29 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Global Macro and UK Election Panel | |

| 165 | 2015.04.22 | New York | IAQF | NYU Kimmel Center | Lasse Pedersen | How Smart Money Invests and Market Prices Are Determined |

| 164 | 2015.04.17 | Budapest | Palack Borbár | Tamas Blummer | Impact of Bitcoin | |

| 163 | 2015.03.25 | London | London Marriott Hotel Canary Wharf | Matthew Dixon | Financial Modelling in Parallel with a High Level Language | |

| 162 | 2015.03.16 | New York | IAQF | NYU Kimmel Center | Travis Fisher | A Numeraire-Independent Fundamental Theorem |

| 161 | 2015.02.23 | London | London Marriott Hotel Canary Wharf | Alexander Denev | Graphical Models for Risk Management and Asset Allocation | |

| 160 | 2015.02.23 | New York | IAQF | NYU Kimmel Center | Roger Lee | Transformations of Volatility Skews into Leveraged Volatility Skews |

| 159 | 2015.02.03 | Geneva | InterContinental Hotel Geneva | Saeed Amen | Thalesians Workshop and AlphaScope Quant Trade Conference | |

| 158 | 2015.01.20 | London | London Marriott Hotel Canary Wharf | Saeed Amen | News Based Systematic Trading of Bonds and FX | |

| 157 | 2015.01.12 | New York | IAQF | NYU Kimmel Center | Andrew Weisman | Liquidations, Fire Sales, and the Cost of Illiquidity |

| 156 | 2014.12.10 | London | La Tasca | Tomas Petricek | Annual Festive Dinner Talk: Deedle: Data and Time Series | |

| 155 | 2014.11.25 | London | London Marriott Hotel Canary Wharf | Tiziana Di Matteo | Structure and Scaling of Financial Time Series | |

| 154 | 2014.11.24 | New York | IAQF | NYU Kimmel Center | Michael Lipkin | The Curious Case of Non-Equilibrium Finance |

| 153 | 2014.11.21 | Budapest | ART IX-XI Gallery | Detlev Schlichter | Paper Money Collapse | |

| 152 | 2014.11.12 | London | London Marriott Hotel Canary Wharf | Damiano Brigo | Optimal Execution | |

| 151 | 2014.11.12 | New York | IAQF | New York Public Library - Science, Industry, and Business | Saeed Amen | Trading Thalesians New York Book Launch |

| 150 | 2014.11.03 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Trading Thalesians London Book Launch | |

| 149 | 2014.10.22 | New York | IAQF | NYU Kimmel Center | Olympia Hadjiliadis | Drawdowns as Insurance and Risk Measures |

| 148 | 2014.10.15 | London | London Marriott Hotel Canary Wharf | Pierre Lequeux | FX Market Structural Changes and Implications | |

| 147 | 2014.09.24 | London | Bloomberg | Bloomberg, City Gate House | Saeed Amen | How Social Media Is Changing News |

| 146 | 2014.09.03 | London | London Marriott Hotel Canary Wharf | Mark Cudmore | Macro Discretionary FX Trading | |

| 145 | 2014.07.25 | Budapest | Palack Borbár | George Cooper | Fixing the Broken Science of Economics | |

| 144 | 2014.07.15 | New York | IAQF | New York Public Library - Science, Industry, and Business | Uwe Naumann | On Adjoint Algorithmic Differentiation |

| 143 | 2014.07.02 | London | London Marriott Hotel Canary Wharf | Saeed Amen | Systematic FX Gamma Trading | |

| 142 | 2014.06.18 | London | London Marriott Hotel Canary Wharf | George Cooper | Herding Cats | |

| 141 | 2014.06.04 | London | London Marriott Hotel Canary Wharf | Haim Bodek | HFT: What's It All About? | |

| 140 | 2014.05.21 | London | London Marriott Hotel Canary Wharf | Tom Wickham-Jones | Coding in the Cloud | |

| 139 | 2014.05.20 | New York | IAQF | NYU Kimmel Center | Peter Carr | Variable Volatility and Financial Failure |

| 138 | 2014.05.19 | Budapest | Palack Borbár | Csaba Toth | Political Risk | |

| 137 | 2014.05.07 | London | London Marriott Hotel Canary Wharf | Iain Clark | Jump Diffusion and Regime Switching Models for Election and FX | |

| 136 | 2014.04.28 | New York | IAQF | NYU Kimmel Center | Allan Malz | Risk-Neutral Systemic Risk Indicators |

| 135 | 2014.04.07 | London | London Marriott Hotel Canary Wharf | Chiara Albanese | Spring Market Views Panel | |

| 134 | 2014.03.26 | London | Dockmaster's House | Didrik Pinte | Python and Quantitative Finance | |

| 133 | 2014.03.20 | New York | IAQF | NYU Kimmel Center | Ciamac Moallemi | High-Frequency Trading and Modern Market Microstructure |

| 132 | 2014.03.12 | London | Dockmaster's House | Vytautas Savickas | Dive into Basis Spreads and FR Replication | |

| 131 | 2014.02.26 | London | Dockmaster's House | Chia Chiang Tan | CVA, DVA, and FVA - Where They Matter | |

| 130 | 2014.02.12 | London | Dockmaster's House | Saeed Amen | Impact of Events on FX Volatility | |

| 129 | 2014.01.31 | Budapest | Palack Borbár | Saeed Amen | Impact of Events on FX Volatility | |

| 128 | 2014.01.29 | London | Dockmaster's House | Katie Martin | Market Views - 5 Year Anniversary | |

| 127 | 2014.01.15 | London | Dockmaster's House | Brian Spector | Implied Volatility Using Python's Pandas Library | |

| 126 | 2014.01.13 | New York | IAQF | NYU Kimmel Center | Marcos López de Prado | On Pseudo-Mathematics and Financial Charlatanism |

| 125 | 2013.12.17 | London | Dockmaster's House | Matthew Dixon | Scalable Financial Computations on Parallel Platforms using Python or R | |

| 125 | 2013.12.17 | London | Dockmaster's House | Mohammad Zubair | Scalable Financial Computations on Parallel Platforms using Python or R | |

| 124 | 2013.12.09 | New York | IAQF | NYU Kimmel Center | Prof. Muthuswamy | Computational Issues in the Near Future for Traders to Ponder |

| 123 | 2013.12.03 | London | Dockmaster's House | Greg Zuckerman | The Frackers | |

| 122 | 2013.11.14 | New York | IAQF | New York Public Library - Science, Industry, and Business | Saeed Amen | The Impact of Scheduled Events on FX Implied Volatility |

| 121 | 2013.11.13 | New York | IAQF | NYU Kimmel Center | Luca Capriotti | Real-time Counterparty Credit Risk Management |

| 120 | 2013.11.06 | London | Dockmaster's House | Saeed Amen | FX Beta, Trading Google, Bloomberg News, and Chinese Data | |

| 119 | 2013.10.16 | London | MSCI | Dockmaster's House | Paul Ward | Manager Crowding and Portfolio Construction |

| 118 | 2013.10.14 | New York | IAQF | NYU Kimmel Center | Antonio Mele | The Price of Fixed Income Market Volatility |

| 117 | 2013.10.02 | London | Dockmaster's House | Tiziana Di Matteo | Financial Markets as Complex Systems | |

| 116 | 2013.09.24 | New York | IAQF | NYU Kimmel Center | Julien Guyon | Particle Method for Solving Your Smile Calibration Problem |

| 115 | 2013.09.18 | London | Dockmaster's House | Cassio Neri | Overview of C++14 | |

| 114 | 2013.09.04 | London | Dockmaster's House | Paul Bilokon | A Brief Introduction to Stochastic Filtering | |

| 113 | 2013.07.16 | New York | New York Public Library - Science, Industry, and Business | Attila Vrabecz | kdb+/q in Practice | |

| 112 | 2013.07.11 | Frankfurt | Quant Finance Germany Group (QFGG) | Atos | Saeed Amen | Currency Hedging of Bonds and Equities |

| 111 | 2013.07.10 | London | Dockmaster's House | Ellie Dobson | Searching for New Physics at the LHC | |

| 110 | 2013.06.26 | London | Dockmaster's House | Uwe Wystup | Overview of Product and Model Trends in FX Options | |

| 109 | 2013.06.19 | New York | IAQF | NYU Kimmel Center | Emilian Belev | Structural Model of Sovereign Credit and Bank Risk |

| 108 | 2013.06.12 | London | Dockmaster's House | Lajos Gergely Gyurko | Modelling and Measuring Slippage | |

| 107 | 2013.06.05 | San Francisco | Quiota | University of San Francisco | Jesse Davis | Risk Model Imposed Manager-to-Manager Correlation |

| 106 | 2013.05.22 | London | Dockmaster's House | Patrick Hagan | Arbitrage-Free SABR | |

| 105 | 2013.05.15 | New York | IAQF | NYU Kimmel Center | Philip Protter | Can One Detect a Bubble in Real-Time? |

| 104 | 2013.05.08 | London | Dockmaster's House | Claudio Albanese | The FVA-DVA Puzzle | |

| 103 | 2013.04.24 | London | Dockmaster's House | Daniel Kuhn | Scenario-Free Stochastic Programming | |

| 102 | 2013.04.23 | New York | IAQF | NYU Kimmel Center | Paul Glasserman | How Likely Is Contagion in Financial Networks? |

| 101 | 2013.04.10 | London | Dockmaster's House | Gary Wong | Margin Lending, Collateral, and CVA Trading | |

| 100 | 2013.03.27 | London | Dockmaster's House | Iain Clark | Commodity Option Pricing: Energy Derivatives | |

| 99 | 2013.03.20 | New York | IAQF | NYU Kimmel Center | Marcos López de Prado | Concealing the Trading Footprint |

| 98 | 2013.03.13 | London | Dockmaster's House | Attila Vrabecz | Financial Data Mining with kdb+/q | |

| 97 | 2013.03.13 | San Francisco | Quiota | Perbacco | Jivendra Kale | Thalesians' San Francisco Dinner Event with Prof. Jivendra Kale |

| 96 | 2013.02.27 | London | Dockmaster's House | Saeed Amen | FX Trading Using Market Positioning in FX | |

| 95 | 2013.02.12 | New York | IAQF | NYU Kimmel Center | Alexander Eydeland | Models in Commodity Markets |

| 94 | 2013.01.14 | New York | IAQF | NYU Kimmel Center | Robert Almgren | Option Hedging with Market Impact |

| 93 | 2012.12.19 | London | Dockmaster's House | Saeed Amen | Annual Festive Dinner Talk: Trading the Impact of Events on FX Implied Volatility | |

| 92 | 2012.11.21 | London | Dockmaster's House | Isabel Ehrlich | Basket Options with Smile | |

| 91 | 2012.11.19 | New York | IAQF | NYU Kimmel Center | Fabio Mercurio | New Challenges in Interest Rate Modelling |

| 90 | 2012.11.07 | London | Dockmaster's House | Gary Wong | Collateral/CVS Trading Issues and Margin Lending | |

| 89 | 2012.10.24 | London | Dockmaster's House | Lars Schouw | Managing Curve Risks in Collateral | |

| 88 | 2012.10.10 | London | Dockmaster's House | Geoffrey Kendrick | Introduction to FX and Beta in FX | |

| 87 | 2012.10.08 | New York | IAQF | NYU Kimmel Center | Philip Maymin | Any Regulation of Risk Increases Risk |

| 86 | 2012.09.26 | London | Dockmaster's House | Rajiv Sosodia | Incorporating Wrong Way Risk in CVA | |

| 85 | 2012.09.18 | New York | IAQF | New York Public Library - Science, Industry, and Business | Saeed Amen | Be Surprised: Growth Surprises and FX Trading |

| 84 | 2012.09.12 | London | Dockmaster's House | Chia Tan | Practical Financial Modelling | |

| 83 | 2012.09.04 | New York | IAQF | NYU Kimmel Center | Michael Kearns | Learning Approaches to Algorithmic Trading |

| 82 | 2012.07.18 | San Francisco | Quiota | Golden Gate University | Richard A. Libby | Liquidity Driven Volatility |

| 81 | 2012.07.04 | London | Dockmaster's House | Saeed Amen | Be Surprised: Growth Surprises and FX Trading | |

| 80 | 2012.06.13 | London | Dockmaster's House | Claudio Albanese | Multi-currency Derivative Portfolios | |

| 79 | 2012.05.30 | London | Dockmaster's House | Saeed Amen | Introduction to FX Momentum and Breakout Trading | |

| 78 | 2012.05.30 | San Francisco | Quiota | Golden Gate University | Jeremy Evnine | Accidental Quant |

| 77 | 2012.05.17 | New York | IAQF | New York Public Library - Science, Industry, and Business | Attilio Meucci | Liquidity-, Funding, and Market-Risk |

| 76 | 2012.05.16 | London | Dockmaster's House | Matthew Dixon | A Bayesian Approach to Discoverying PE | |

| 75 | 2012.05.02 | San Francisco | Quiota | Golden Gate University | Walter Tackett | Tutorial on the Analysis of Implicit Views |

| 74 | 2012.04.11 | London | Dockmaster's House | Max Little | A Functional Minimization Approach to Level Shift Detection | |

| 73 | 2012.03.29 | New York | IAQF | Baruch College | Mike Lipkin | Event Driven Finance |

| 72 | 2012.03.28 | London | Dockmaster's House | Oleg Ruban | Scenarios for Sovereign Stress in Eurozone | |

| 71 | 2012.03.14 | London | City Pride | Attila Vrabecz | kdb+/q in Practice | |

| 70 | 2012.03.07 | San Francisco | Quiota | Golden Gate University | Lisa Goldberg | Contractual Tail Risk Hedging |

| 69 | 2012.02.22 | London | City Pride | Sergey Nadtochiy | Static Hedging of Barrier Options | |

| 68 | 2012.02.08 | San Francisco | Quiota | Golden Gate University | Alper Atamturk | Conic Optimization for Portfolios and Risk |

| 67 | 2012.01.31 | New York | IAQF | New York Public Library - Science, Industry, and Business | Harvey Stein | Counterparty Risk, CDS, and CCDS |

| 66 | 2012.01.25 | London | City Pride | Iain Clark | Foreign Currency Options: Deltas, Markets, Smile | |

| 65 | 2012.01.25 | San Francisco | Quiota | Golden Gate University | Jose Menchero | Eigenfactor Risk Adjustments |

| 64 | 2012.01.11 | London | City Pride | Saeed Amen | Currency Hedging of Bonds and Equities | |

| 63 | 2012.01.11 | San Francisco | Quiota | Golden Gate University | Lisa Goldberg | Contractual Tail Risk Hedging |

| 62 | 2011.12.14 | San Francisco | Quiota | Golden Gate University | Farshid Jamshidian | An Overview of Interest-Rate Derivatives Modelling |

| 61 | 2011.12.07 | London | City Pride | Saeed Amen | Festive Dinner Talk: What Drives Gold? | |

| 60 | 2011.11.30 | London | City Pride | Boryana Racheva-Iotova | Fat-Tailed Risk Models | |

| 59 | 2011.11.30 | San Francisco | Quiota | Golden Gate University | Peter G. Shepard | On 2nd Order Risk |

| 58 | 2011.11.02 | London | City Pride | Cassio Neri | Introduction to the KeyValue Library | |

| 57 | 2011.10.19 | London | City Pride | Uwe Wystup | Embedded Currency Options in Roll-Over Loans | |

| 56 | 2011.10.19 | San Francisco | Quiota | Golden Gate University | Richard A. Libby | Metamathematical Finance |

| 55 | 2011.10.05 | London | City Pride | John Crosby | Tradng and Hedging Complex Derivatives | |

| 54 | 2011.09.14 | London | City Pride | Lajos Gergely Gyurko | Cubature on Wiener Space and Multilevel Monte Carlo | |

| 53 | 2011.08.23 | New York | IAQF | New York Public Library - Science, Industry, and Business | Greg Zuckerman | Lessons from the Greatest Trade Ever |

| 52 | 2011.07.13 | London | City Pride | Saeed Amen | US Employment Report and Impact on Intraday FX | |

| 51 | 2011.06.29 | New York | IAQF | O'Lunneys | Rakesh Joshi | FPGAs in HFT |

| 50 | 2011.06.15 | London | City Pride | Claudio Albanese | Counterparty Credit Risk Strategies | |

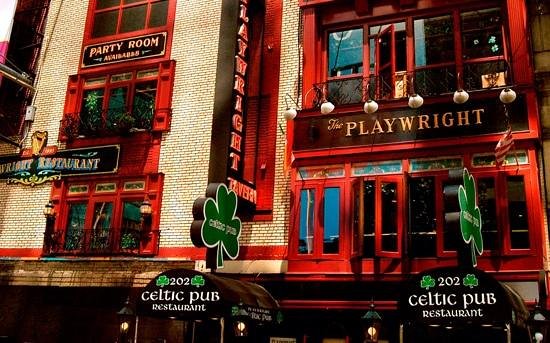

| 49 | 2011.06.14 | New York | IAQF | Playwright Tavern | Jim Gatheral | Optimal Order Execution |

| 48 | 2011.06.07 | New York | IAQF | Playwright Tavern | Claudio Albanese | Counterparty Credit Risk Strategies |

| 47 | 2011.05.25 | London | City Pride | Greg Zuckerman | Lessons from the Greatest Trade Ever | |

| 46 | 2011.05.04 | London | City Pride | Chia Tan | Structured Products and the Economic Environment | |

| 45 | 2011.04.20 | London | City Pride | Tom Wickham-Jones | High Performance Computing Using Mathematica | |

| 44 | 2011.04.06 | London | City Pride | Henrik Jensen | Complexity Science in Finance | |

| 43 | 2011.03.30 | San Francisco | Quiota | L'Olivier French Restaurant | Saeed Amen | US Employment Report and Impact on Intraday FX |

| 42 | 2011.03.16 | London | Maxeler | City Pride | Mike Flynn | Vertical Acceleration of Financial Algorithms |

| 41 | 2011.03.09 | New York | IAQF | Playwright Tavern | Peter Decrem | Interest Rate and Credit Modelling on GPUs |

| 40 | 2011.02.23 | New York | IAQF | Playwright Tavern | Gerald Hanweck, Jr. | Monte Carlo Methods in CUDA |

| 39 | 2010.12.01 | London | City Pride | Alex Langnau | Local Correlation Modelling | |

| 38 | 2010.11.24 | London | City Pride | Iain Clark | Book Presentation: FX Options | |

| 37 | 2010.11.03 | London | MWB Canary Wharf | Patrick Hagan | Masterclass: Managing Smile Risk and Exotics | |

| 36 | 2010.11.02 | London | City Pride | Patrick Burns | Effective Backtesting | |

| 35 | 2010.10.27 | London | City Pride | Vincent Hindriksen | On the Usability of OpenCL | |

| 34 | 2010.10.20 | London | City Pride | Egor Avdeev | Fixed-Income Relative Value Trading | |

| 33 | 2010.10.07 | London | MWB Canary Wharf | Dan Crisan | Masterclass: Introduction to Stochastic Calculus | |

| 32 | 2010.09.22 | London | City Pride | Mike Staunton | Portable Code: FFT Option Pricing | |

| 31 | 2010.09.08 | London | City Pride | Frank Berkshire | A Primer on Risk and Gambler's Ruin | |

| 30 | 2010.08.02 | London | Idea Store Canary Wharf | Paul Bilokon | Study Group: Stochastic Calculus | |

| 29 | 2010.07.05 | London | Idea Store Canary Wharf | Paul Bilokon | Study Group: Stochastic Calculus | |

| 28 | 2010.06.30 | London | City Pride | Attila Vrabecz | kdb+/q: A Perfect Tool for Your Data | |

| 27 | 2010.06.21 | London | Idea Store Canary Wharf | Paul Bilokon | Study Group: Stochastic Calculus | |

| 26 | 2010.06.02 | London | City Pride | Saeed Amen | Candlestick Trading in FX | |

| 25 | 2010.05.05 | London | City Pride | Lynda White | Collaborative Games with n Players | |

| 24 | 2010.04.07 | London | City Pride | Sundararajan Srinivasa | Behavioural Trading | |

| 23 | 2010.03.24 | London | City Pride | David Barrie Thomas | FPGAs for Financial Computing? | |

| 22 | 2010.03.15 | London | MWB Canary Wharf | Dan Crisan | Introduction to Stochastic Calculus | |

| 21 | 2010.03.10 | London | City Pride | Iain Clark | Local and Stochastic Volatility | |

| 20 | 2010.03.08 | London | City Pride | Attilio Meucci | Managing Diversification | |

| 19 | 2010.02.10 | London | City Pride | Saeed Amen | Examining the Intraday Impact of Rates Decisions on G10 FX | |

| 18 | 2009.12.15 | London | NAG | City Pride | Robert Tong | Monte Carlo Simulation and Its Efficient Implementation |

| 18 | 2009.12.15 | London | NAG | City Pride | Kai Zhang | Monte Carlo Simulation and Its Efficient Implementation |

| 17 | 2009.12.02 | London | City Pride | Sverlozar (Zari) T. Rachev | Market Crashes and Modelling Volatile Markets | |

| 16 | 2009.11.30 | London | City Pride | Peter Carr | Local Variance Gamma | |

| 15 | 2009.11.24 | London | City Pride | Steve Zymler | Worst-Case VaR of Derivative Portfolios: A Cure for Black Swans? | |

| 14 | 2009.11.18 | London | City Pride | Kevin Parrott | ||

| 13 | 2009.10.21 | London | City Pride | Saeed Amen | Intraday Impact of Economic Data Releases on the Australian Dollar | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Claudio Albanese | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Thomas Bradley | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Mike Giles | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Paul Kelly | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | David Thomas | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Robert Tong | Thalesian Workshop 2009: GPUs in Finance | |

| 12 | 2009.09.11 | London | Department of Computing, Imperial College London | Gernot Ziegler | Thalesian Workshop 2009: GPUs in Finance | |

| 11 | 2009.08.19 | London | City Pride | Aly Kassam | Implementing High Frequency Trading Algorithms Ten Times Faster | |

| 10 | 2009.07.22 | London | City Pride | Dan Crisan | Solving Backward SDEs using Cubature Methods | |

| 9 | 2009.07.07 | London | City Pride | Rene Reinbacher | Markovian Projection, Heston Model and Pricing on a Smile | |

| 8 | 2009.06.17 | London | City Pride | Adrian Zymolka | Mastering Constraints for Portfolio Construction | |

| 7 | 2009.06.03 | London | City Pride | Patrick Burns | Using Random Portfolios with R | |

| 6 | 2009.05.20 | London | City Pride | David Bellot | Introduction to Probabilistic Decision Support for Automatic Trading | |

| 5 | 2009.04.28 | London | City Pride | Gernot Ziegler | CUDA - GPU Computing for Financial Applications | |

| 5 | 2009.04.28 | London | City Pride | Thomas Bradley | CUDA - GPU Computing for Financial Applications | |

| 4 | 2009.03.25 | London | City Pride | Berc Rustem | Robustness in Investment Decisions | |

| 4 | 2009.03.25 | London | City Pride | Steve Zymler | Robustness in Investment Decisions | |

| 3 | 2009.03.04 | London | City Pride | Claudio Albanese | Interest Rate Derivatives and GPU Computing | |

| 2 | 2009.02.11 | London | City Pride | Saeed Amen | Introduction to Foreign Exchange | |

| 1 | 2009.01.29 | London | City Pride | Matthew Dixon | Calibrating Spread Options using a Seasonal Commodity Forward Model |

The Thalesian Seminars take place at some of the most prestigious venues, including Level39, City University Club, and London Marriott Hotel Canary Wharf (pictured) in London; Fordham University Gabelli School of Business and NYU Kimmel Center in New York City; and central locations in Budapest, Frankfurt, Geneva, Prague, San Francisco, Stockholm, Vienna, and Zurich.

More than 300 Thalesian Seminars have taken place around the world.

During the COVID-19 pandemic we have made the decision to switch to the webinar mode—the Thalesian Webinars are currently taking place online. The same decision has been made by our partners in New York—IAQF. In New York the Seminar/Webinar series is known as IAQF/Thalesians.

Some of the venues associated with the Thalesian Seminars have taken their due place in history. The very first Seminar (Prof. Matthew Dixon’s talk entitled Calibrating Spread Options using a Seasonal Commodity Forward Model) took place upstairs at the City Pride pub on 2009.01.29.

The City Pride was situated at 1 Westferry Road in Marsh Wall on the Isle of Dogs, London. This pub was built in 1936 as the City Arms, with a name change to the City Pride in 1988. It closed in 2010.05m and was demolished in 2012.10m. The site is now occupied by the Landmark Pinnacle, a 233-metre (764 ft) skyscraper under construction by developer Chalegrove Properties. Is is set to be the tallest residential building in Europe and will have more habitable floors than any other building in Europe. The 71st Thalesian Seminar on 2012.03.14 was the last one to take at the old City Pride. It was given by Attila Vrabecz and was entitled kdb+/q in Practice.

The London Chapter of the Thalesians then moved to the Dockmaster’s House. This listed Georgian building constructed in 1807 has had many past incarnations; it’s been an excise office, a pub called the Jamaica Tavern renamed as the Jamaica Hotel in 1899, and even the offices for the Dock Superintendent and his staff from 1926—hence the name given to it in 1992. From February 2009, it opened as an Indian restaurant, with dining rooms, three bars, and a garden with a stylish conservatory. The first Thalesian seminar to take place at the Dockmaster’s House was the 72nd one; it was given on 2012.03.28 by Oleg Ruban, entitled Scenarios for Sovereign Stress in Eurozone.

While the building still stands, the restaurant closed its doors in 2014. The last Thalesian talk was given at that venue on 2014.03.26 by Didrik Pinte—it was entitled Python and Quantitative Finance.

The London seminar series then moved to the London Marriott Hotel Canary Wharf, which was at the time known as the London Marriott West India Quay. The venue was inaugurated on 2014.04.07 by Chiara Albanese; it was a panel talk, Spring Market Views Panel.

The Thalesians’ success in Canary Wharf prompted us to expand to the City of London. We were invited by the Secretary of the City University Club, Hasita Senanayake FIH, to use the Club as a venue alongside the London Marriott Hotel Canary Wharf. The first talk at the new venue was given on 2017.03.09 by Iain Clark—Efficient Methods for Simulation of FX Volatility Surface.

The City University Club was established in 1895. From its foundation until 2018 it operated from the top three floors of 50 Cornhill, of what was Prescott’s Bank, a 1766 private bank which became a branch of part of the NatWest banking group. This arrangement was quite specifically intended by and between the bank’s partners and the club of which they were founding members when the building was designed. The branch closed in 1999 and was turned into a pub of the Fullers chain.

On 2018.01.29 the Club moved to 42 Crutched Friars, the former home of the Lloyds Club. The last Thalesian Seminar at 50 Cornhill was given on 2017.11.09 by Blanka Horvath—Rough Volatility Models: Pricing and Simulations. The first Thalesian Seminar at the Club’s new location was given on 2018.06.13 by Ian Khrashchevskyi—Is There a Reward for Macroeconomic Risk in Higher Moment Risk Premia?

On 2011.02.23 the IAQF/Thalesian Seminar series launched in New York City at the Playwright Tavern. The person behind the New York IAQF/Thalesians series is Dr Harvey Stein. The IAQF is the not-for-profit, professional society dedicated to fostering the profession of quantitative finance by providing platforms to discuss cutting-edge and pivotal issues in the field. Founded in 1992, the IAQF is composed of individual academics and practitioners from banks, broker dealers, hedge funds, pension funds, asset managers, technology firms, regulators, accounting, consulting, and law firms, and universities across the globe. The first IAQF/Thalesian seminar was given by Gerald Hanweck, Jr. It was entitled Monte Carlo Methods in CUDA.

The 51st IAQF/Thalesian Seminar took place at O’Lunney’s. It was given on 2011.06.29 by Rakesh Joshi on the subject of FPGAs in HFT.

From 2011.08.23 onwards the IAQF/Thalesian Seminars in New York City took place at the New York Public Library, Baruch College, and NYU Kimmel Center. There have been few exceptions. For example, the 180th Seminar took place at the Shark Tank, Grind Broadway (Saeed Amen, Creating Trend Following Fund / PyThalesians Demo), whereas the 247th Seminar took place at the Bank of China (Lasse Pedersen, Generalized Recovery). More recent IAQF/Thalesian Seminars took place at Fordham University Gabelli School of Business.

The Thalesian Seminars—or Séances, as they are referred to in Hungary—in Budapest started on 2014.01.31 at Palack Borbár. In Frankfurt, they started on 2013.07.11 at Atos, moved to Die Zentrale on 2015.06.03, and then to PPI AG Office on 2015.09.07. In Geneva—on 2015.02.03 at InterContinental Hotel Geneva; in Prague—on 2015.05.29 at the Konferenční sály Akademie věd ČR; in San Francisco on 2011.03.30 at L’Olivier (moving to Golden Gate University on 2011.10.19 and to Berkeley City Club on 2015.09.10); in Stockholm on 2017.04.26 at the Kräftriket; in Vienna on 2018.05.28 at the University of Vienna; in Zurich on 2015.09.08 at the ETH Swiss Federal Institute of Technology.

The following people have contributed to the worldwide Thalesian seminars: Attila Agod (Budapest), Saeed Amen (London), Fazlynn Azrul (London), Paul Bilokon (London), Matthew Dixon (San Francisco), Swati Mital (Zurich), Pavel Motuzenko (Zurich), Jan Novotny (Prague), Jörg Osterrieder (Frankfurt), Jochen Papenbrock (Frankfurt), Hans-Peter Schrei (Vienna), Peter Schwender (Frankfurt), Harvey Stein (New York), Richard Warnung (Vienna), Adrian Zymolka (Frankfurt).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}